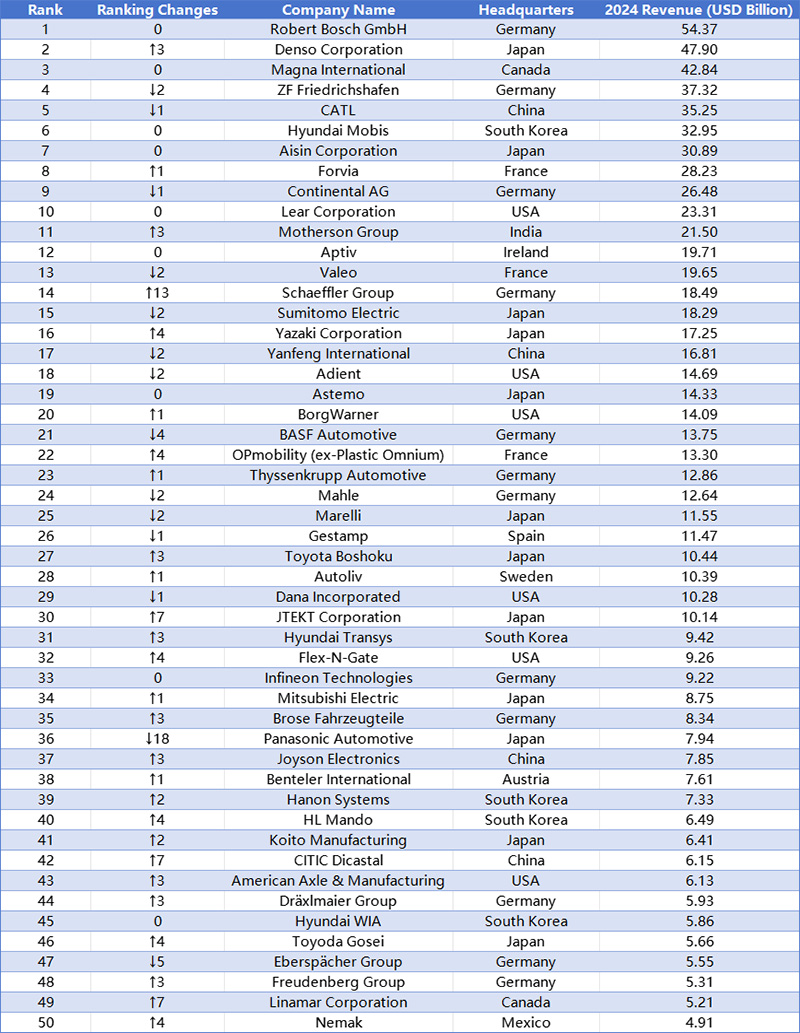

Top 50 Global Auto Parts Supply Chain Companies in 2025

From 2024 to 2025, the global automotive parts industry faces a severe market landscape: global automobile sales growth stagnates, the penetration rate of pure electric vehicles has not met expectations, software costs continue to rise, but consumers' demand for intelligent driving assistance systems (ADAS) and intelligent network functions is still increasing; China's economic growth slowdown has led to intensified competition in the automobile market; geopolitical tensions are increasing, and global trade barriers are rising again.

Against this background, global automotive parts companies also face the challenges of technological and business model transformation, cost pressures are rising sharply, and they continue to face profitability challenges, which is also reflected in the financial performance of companies.

According to the 2025 Global Automotive Parts Suppliers Top 100 List released by Automotive News on June 23, under the above multiple challenges, the ranking of the list has been shuffled violently-60% of the parts companies have experienced varying degrees of sales decline, and even top-level parts giants such as Bosch and ZF are not immune.

However, there are also some suppliers that stand out against the trend: the sales of most Chinese suppliers have increased compared with the same period last year, among which Ningbo Top and Desay SV have risen strongly, climbing 21 and 16 places in the ranking respectively, which is remarkable.

Key Trends:

Chinese Suppliers Rising – CATL (#5), Yanfeng (#17), Joyson (#37), and CITIC Dicastal (#42) show strong growth.

Market Slowdown – Overall revenue declined by 3.5% due to EV transition challenges.

Regional Dominance – Japan (22), USA (18), Germany (16), and China (15) lead in representation.

Data from this year's list shows that as the global automotive parts industry enters a "stagnation and transformation period", 60% of parts suppliers will see a year-on-year decline in sales in 2024, causing the total global sales of suppliers on the list this year to fall by 7% year-on-year compared to 2023.

In 2023, five suppliers had automotive business revenues exceeding $40 billion, while only three did so in 2024.

The development of electric vehicles is not as expected, and the performance differentiation of related suppliers is intensifying

In the past two years, with the continued growth of the global electric vehicle market, electric vehicle battery and other related parts manufacturers have become a regular on the list of the top 100 global automotive parts suppliers.

However, as the uncertainty of electric vehicle market policies and regulations has increased, the development speed of electric vehicles in the European and American markets has gradually fallen short of expectations. Some automakers have postponed, reduced or even cancelled major electric vehicle projects, which has led to lower electric vehicle-related revenues than many suppliers expected; at the same time, because suppliers have made costly investments, but the return on expenditures has been lower than expected, resulting in stranded funds and declining profits.

SK On, a South Korean lithium-ion battery manufacturer, is a typical example. The company has added several production bases in North America, a key strategic region, but due to the retreat of several major US automakers on electric vehicle plans, its sales in 2024 fell by 54% year-on-year, and its ranking dropped by 21 places from 2023, making it the company with the largest decline in the top 100 list. The company directly attributes this to the reduction in global demand for electric vehicles.

Diverging results among leading battery makers underscore the EV market's complexity and the challenge of forecasting component revenues. Over the last 18 months, the electric drivetrain landscape has pivoted toward a more diverse range of technologies beyond pure BEVs. In North America, shifting trade policies and regulatory uncertainty have left suppliers hesitant to invest. ZF now expects global EV penetration to reach only 39% by 2031—down from an earlier 55% estimate—with the U.S. market splitting evenly between EVs, hybrids, and gas cars. Leading suppliers now emphasize that ICE components remain a core profit driver, while hybrids are poised for sustained growth in the U.S. and China.

EC-6100 Automatic Heat Shrink Tube Cutting Machine EC-6800 Automatic Cutting Machine EC-6100H Automatic Hot Cutting Machine EC-830 Corrugated Tube Cutting Machine EC-6500 Automatic Cable and Tube Cutting Machine EC-810 Automatic Cable Cutting Machine EC-850X Automatic Rotary Cutting Machine EC-821 Corrugated Tube Cutting Machine EC-890 Multifunctional Automatic Cutting Machine EC-870 High-power Automatic Tube Cutting Machine EC-816 Automatic Cutting Machine EC-823 High Speed Cutting Machine EC-805 Automatic Cable Cutting Machine EC-860 Corrugated Tube Cutting Machine EC-830F Automatic Tube Cutting Machine With Feeding System EC-830FS Tube Cutting Machine With Feeding System EC-3100 Automatic Cable and Tube Cutting Machine

EC-6100 Automatic Heat Shrink Tube Cutting Machine EC-6800 Automatic Cutting Machine EC-6100H Automatic Hot Cutting Machine EC-830 Corrugated Tube Cutting Machine EC-6500 Automatic Cable and Tube Cutting Machine EC-810 Automatic Cable Cutting Machine EC-850X Automatic Rotary Cutting Machine EC-821 Corrugated Tube Cutting Machine EC-890 Multifunctional Automatic Cutting Machine EC-870 High-power Automatic Tube Cutting Machine EC-816 Automatic Cutting Machine EC-823 High Speed Cutting Machine EC-805 Automatic Cable Cutting Machine EC-860 Corrugated Tube Cutting Machine EC-830F Automatic Tube Cutting Machine With Feeding System EC-830FS Tube Cutting Machine With Feeding System EC-3100 Automatic Cable and Tube Cutting Machine CS-4507/6010 Multifunctional Wire Stripping Machine UniStrip 2016 Pneumatic Wire Stripping Machine UniStrip 2018E Electric Cable Wire Stripping Machine CS-5507 Automatic Coaxial Cable Stripping Machine CS-5515 Automatic coaxial cable stripping machine CS-400 Braided Shield Cable Stripping Machine CS Series Rotary Cable Stripping Machine CS-2486 Coaxial Cable Wire Stripping Machine

CS-4507/6010 Multifunctional Wire Stripping Machine UniStrip 2016 Pneumatic Wire Stripping Machine UniStrip 2018E Electric Cable Wire Stripping Machine CS-5507 Automatic Coaxial Cable Stripping Machine CS-5515 Automatic coaxial cable stripping machine CS-400 Braided Shield Cable Stripping Machine CS Series Rotary Cable Stripping Machine CS-2486 Coaxial Cable Wire Stripping Machine TM-20 Terminal Crimping Machine TM-20S Automatic Wire Terminal Crimping Machine TM-200 Terminal Crimping Machine TM-10P Registered Jack Crimping Machine TM-E140 Pre-insulation Ferrule Terminal Strip And Crimp Machine TM-E140S Automatic Wire Stripping Ferrule Crimping Machine TM-P300 Pneumatic Terminal Crimping Machine TM-E116 Electric Terminal Crimping Machine TM-P120 Pneumatic Terminal Crimping Machine SAT-AS6P Pneumatic Crimping Applicator SAT-MS6 Mechanical Crimping Applicator Side Feed Terminal Crimping Applicator Rear Feed Terminal Crimping Applicator Flag Terminal Crimping Applicator Crimp Applicator for Insulated Terminals TM-T Series Intelligent Servo Terminal Crimping Machine SAT-MS5 OTP Mechanical Applicator TM-25M Automatic Terminal Crimping Machine TM-FK40 Terminal Crimping Machine TM-CS6 Ultra Silent Copper Belt Crimping Machine

TM-20 Terminal Crimping Machine TM-20S Automatic Wire Terminal Crimping Machine TM-200 Terminal Crimping Machine TM-10P Registered Jack Crimping Machine TM-E140 Pre-insulation Ferrule Terminal Strip And Crimp Machine TM-E140S Automatic Wire Stripping Ferrule Crimping Machine TM-P300 Pneumatic Terminal Crimping Machine TM-E116 Electric Terminal Crimping Machine TM-P120 Pneumatic Terminal Crimping Machine SAT-AS6P Pneumatic Crimping Applicator SAT-MS6 Mechanical Crimping Applicator Side Feed Terminal Crimping Applicator Rear Feed Terminal Crimping Applicator Flag Terminal Crimping Applicator Crimp Applicator for Insulated Terminals TM-T Series Intelligent Servo Terminal Crimping Machine SAT-MS5 OTP Mechanical Applicator TM-25M Automatic Terminal Crimping Machine TM-FK40 Terminal Crimping Machine TM-CS6 Ultra Silent Copper Belt Crimping Machine ESC-BX1 Wire Cutting and Stripping Machine ESC-BX4 Wire Cutting And Stripping Machine ESC-BX30 Automatic Large Cable Cutting and Stripping Machine ESC-BX30S Sheathed Cable Automatic Cutting and Stripping Machine ESC-BXR Automatic Rotary Cable Stripping Machine ESC-BX6 Wire Cutting And Stripping Machine ESC-BX7 Wire Cutting And Stripping Machine ESC-BX8S Sheath Cable Cutting and Stripping Machine ESC-BX8PR Wire Cutting And Stripping Machine ESC-BX9 Automatic Cut and Strip Machine ESC-BX30SC Automatic Cable Wire Cutting and Stripping Machine ESC-BX120 Automatic Cutting and Stripping Machine ESC-BX30RS Multi-function Rotary Cable Stripping Machine ESC-BX120S Multi-core Cable Cutting and Stripping Machine ESC-BX60 Automatic Cable Cutting and Stripping Machine CS-9685 Coaxial Cable Cutting and Stripping Machine CS-9680 Automatic Coaxial Cable Stripping Machine ESC-BX300 Automatic Cable Wire Cutting And Stripping Machine ESC-BX16 Wire Cutting Stripping Machine ESC-BX20SF Flat Twin Wire Cutting and Stripping Machine

ESC-BX1 Wire Cutting and Stripping Machine ESC-BX4 Wire Cutting And Stripping Machine ESC-BX30 Automatic Large Cable Cutting and Stripping Machine ESC-BX30S Sheathed Cable Automatic Cutting and Stripping Machine ESC-BXR Automatic Rotary Cable Stripping Machine ESC-BX6 Wire Cutting And Stripping Machine ESC-BX7 Wire Cutting And Stripping Machine ESC-BX8S Sheath Cable Cutting and Stripping Machine ESC-BX8PR Wire Cutting And Stripping Machine ESC-BX9 Automatic Cut and Strip Machine ESC-BX30SC Automatic Cable Wire Cutting and Stripping Machine ESC-BX120 Automatic Cutting and Stripping Machine ESC-BX30RS Multi-function Rotary Cable Stripping Machine ESC-BX120S Multi-core Cable Cutting and Stripping Machine ESC-BX60 Automatic Cable Cutting and Stripping Machine CS-9685 Coaxial Cable Cutting and Stripping Machine CS-9680 Automatic Coaxial Cable Stripping Machine ESC-BX300 Automatic Cable Wire Cutting And Stripping Machine ESC-BX16 Wire Cutting Stripping Machine ESC-BX20SF Flat Twin Wire Cutting and Stripping Machine ACC-101 Automatic Single-head Terminal Crimping Machine ACC-102A Fully Automatic Terminal Crimping Machine (Both Ends) ACC-102B Automatic Double Terminal Crimping Machine ACC-105 Fully Automatic Single-head End-dipping Tin Machine ACC-106 Fully Automatic 5-Wire Single-head End-dipping Tin Machine ACC-202UP Fully-automatic cut,strip,crimp,insert and Heat Heat-shrink tube machine ACC-308 (Both ends) Full automatic Soldering machine ACC-208 Fully Automatic Crimping Machine (Both Ends) ACC-508 Fully Automatic Twisting, Soldering and Crimping Machine ACC-608 Fully Automatic Flat Cable Cut Strip and Crimp Machine

ACC-101 Automatic Single-head Terminal Crimping Machine ACC-102A Fully Automatic Terminal Crimping Machine (Both Ends) ACC-102B Automatic Double Terminal Crimping Machine ACC-105 Fully Automatic Single-head End-dipping Tin Machine ACC-106 Fully Automatic 5-Wire Single-head End-dipping Tin Machine ACC-202UP Fully-automatic cut,strip,crimp,insert and Heat Heat-shrink tube machine ACC-308 (Both ends) Full automatic Soldering machine ACC-208 Fully Automatic Crimping Machine (Both Ends) ACC-508 Fully Automatic Twisting, Soldering and Crimping Machine ACC-608 Fully Automatic Flat Cable Cut Strip and Crimp Machine HSM-60 Heat Shrink Tube Processing Machine HSM-70 Heat Shrink Tube Processing Machine HSM-80B Heat Shrink Tube Processing Machine HSM-90 Heat Shrink Tube Processing Machine HSM-25M Heat Shrink Tube Processing Machine HSM-120 Heat Shrink Tube Heating Machine HSM-50 Heat Shrink Tube Processing Machine HSM-160 Heat Shrink Tube Processing Machine HSM-80A Heat Shrink Tube Heating Machine HSM-260E Enclosed Heat Shrink Tube Processing Machine HSM-260O Open Heat Shrink Tube Processing Machine HSM-20 Intelligent Heat Shrink Tube Processing Machine

HSM-60 Heat Shrink Tube Processing Machine HSM-70 Heat Shrink Tube Processing Machine HSM-80B Heat Shrink Tube Processing Machine HSM-90 Heat Shrink Tube Processing Machine HSM-25M Heat Shrink Tube Processing Machine HSM-120 Heat Shrink Tube Heating Machine HSM-50 Heat Shrink Tube Processing Machine HSM-160 Heat Shrink Tube Processing Machine HSM-80A Heat Shrink Tube Heating Machine HSM-260E Enclosed Heat Shrink Tube Processing Machine HSM-260O Open Heat Shrink Tube Processing Machine HSM-20 Intelligent Heat Shrink Tube Processing Machine HV-CS 9070 High-Voltage Cable Shield Cutting Machine HV-FS 9053 Cable Shield Folding Machine HV-ACS 9100 Cable Shield Processing Machine HV-ACS 9200 Automatic Cable Shield Processing System HV-ACS 9300 Automotive High Voltage Cable Processing Machine HV-ACS 9500 High Voltage Cable Processing Machine HV-FC 9312 Aluminum Foil Cutting Machine HV-CS 9120 Cable Stripping Machine

HV-CS 9070 High-Voltage Cable Shield Cutting Machine HV-FS 9053 Cable Shield Folding Machine HV-ACS 9100 Cable Shield Processing Machine HV-ACS 9200 Automatic Cable Shield Processing System HV-ACS 9300 Automotive High Voltage Cable Processing Machine HV-ACS 9500 High Voltage Cable Processing Machine HV-FC 9312 Aluminum Foil Cutting Machine HV-CS 9120 Cable Stripping Machine STB-10 Automatic Tape Bundling Machine STB-50 Desktop Bundling Machine STB-60 Adhesive Tape Bundling Machine STB-55 Desktop Tape Bundling Machine STB-50C Automatic Tape Cutting Machine STP-B Hand-held Taping Machine STP-F Hand-held Lithium Battery Tape Wrapping Machine STP-C Automatic Wire Taping Machine STP-D Automatic Tape Wrapping Machine STP-AS Automatic Tape bundling Machine

STB-10 Automatic Tape Bundling Machine STB-50 Desktop Bundling Machine STB-60 Adhesive Tape Bundling Machine STB-55 Desktop Tape Bundling Machine STB-50C Automatic Tape Cutting Machine STP-B Hand-held Taping Machine STP-F Hand-held Lithium Battery Tape Wrapping Machine STP-C Automatic Wire Taping Machine STP-D Automatic Tape Wrapping Machine STP-AS Automatic Tape bundling Machine CB-B15 Automatic Wiring Winding Machine CB-BT15 Automatic Wiring Winding Binding Machine CB-F30/150MCS Automatic Wiring Winding Machine CB-F30/150MCST18-45 Automatic Wiring Winding Binding Machine CB-F30/150MCST40-80 Automatic Wiring Winding Binding Machine CB-B15CST Automatic Wiring Coiling Binding Machine CB-F500MCS Automatic Wiring Winding Machine CB-B30/150CS Automatic Wiring Winding Machine CB-B10/15CS Automatic Wiring Winding Machine CB-WT630 Automatic Wire Winding and Tying Machine

CB-B15 Automatic Wiring Winding Machine CB-BT15 Automatic Wiring Winding Binding Machine CB-F30/150MCS Automatic Wiring Winding Machine CB-F30/150MCST18-45 Automatic Wiring Winding Binding Machine CB-F30/150MCST40-80 Automatic Wiring Winding Binding Machine CB-B15CST Automatic Wiring Coiling Binding Machine CB-F500MCS Automatic Wiring Winding Machine CB-B30/150CS Automatic Wiring Winding Machine CB-B10/15CS Automatic Wiring Winding Machine CB-WT630 Automatic Wire Winding and Tying Machine PF-820 Wire Prefeeding Machine PF-08 Automatic Wire Prefeeder PF-30 Automatic Prefeeding Machine PF-60 Automatic Prefeeding Machine PF-150 Automatic Wire Prefeeding Machine CC-380 Cable Coiling Machine CC-680 Automatic Cable Coiling Machine CC-380D Cable Coil Machine PF-120 Large Automatic Wire Prefeeding Machine PF-90 Automatic Wire Prefeeder PF-100 Automatic Prefeeder PF-04 Automatic Wire Prefeeder PF-06 Automatic Wire Prefeeder PF-05 Automatic Wire Prefeeder

PF-820 Wire Prefeeding Machine PF-08 Automatic Wire Prefeeder PF-30 Automatic Prefeeding Machine PF-60 Automatic Prefeeding Machine PF-150 Automatic Wire Prefeeding Machine CC-380 Cable Coiling Machine CC-680 Automatic Cable Coiling Machine CC-380D Cable Coil Machine PF-120 Large Automatic Wire Prefeeding Machine PF-90 Automatic Wire Prefeeder PF-100 Automatic Prefeeder PF-04 Automatic Wire Prefeeder PF-06 Automatic Wire Prefeeder PF-05 Automatic Wire Prefeeder

CHM-10 Crimp-Height Measurer PFM-220 Terminal Pulling Force Tester PFM-300 Terminal Pulling Force Tester PFM-200 Pull Force Tester For Wire Terminals TCA-120 Terminal Cross Section Analyzer TCA-120S Terminal Cross Section Analyzer TCA-150 Terminal Cross Section Analyzer PFM-50 Pull Force Measuring Machine

CHM-10 Crimp-Height Measurer PFM-220 Terminal Pulling Force Tester PFM-300 Terminal Pulling Force Tester PFM-200 Pull Force Tester For Wire Terminals TCA-120 Terminal Cross Section Analyzer TCA-120S Terminal Cross Section Analyzer TCA-150 Terminal Cross Section Analyzer PFM-50 Pull Force Measuring Machine